| | PAEs | NPAEs |

Financial Statements | – Comprehensive Income Statement | – Profit and Loss Statement (P&L) |

– Cash Flow Statement | – statement of comprehensive income (non-disclosure of specific expenses). |

– statement of financial position (3-period balance sheet) | |

–income statement (mandatory disclosure of significant expenses and additional disclosure of expenses by nature). | |

Investment capital | – cost of sales | – cost deducted by provision for depreciation |

–fair value (trading/securities held for sale). | – fair value adjustments through profit or loss and other comprehensive income. |

Investment in subsidiaries. | – Financial statements must be prepared and recognition of profit/loss must be in accordance with the revenue and expense recognition principles. | –No need to prepare consolidated financial statements and record cost prices. |

Employee benefits. | – Calculation must be based on actuarial mathematics standards. | – Calculate using an estimation method, which the Auditor deems reasonable. |

Intangible Assets | – No need for disposal (similar to depreciation calculation), by examining whether there is impairment at the end of the year or not. | – Disposal after 10 years. |

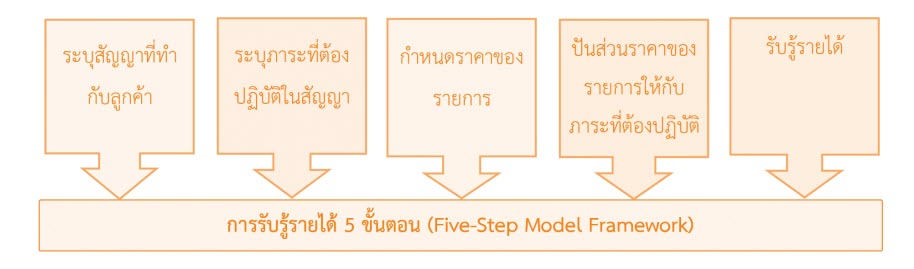

Recognize revenue. | – According to TFRS 15’s 5-step process. | – Recognize revenue when control is transferred or at a point where risks and rewards are transferred and revenue is recognized. |

Income from real estate sales | – Revenue is recognized upon transfer. | – Can choose 3 Options |

| | 1. Receiving income upon transfer |

| | 2. Understanding income based on the proportion of successfully completed work |

| | 3. Understanding income based on installment payments transferred when due |

Income TAX | –Calculating deferred tax assets due to differences between accounting and tax, which may result in assets/liabilities, income tax, or deferred tax assets (DTA)/deferred tax liabilities (DTL). | – No need to calculate, just record the accrued Income TAX. |